Featured

Table of Contents

- – Not known Details About Financial Implications...

- – The Of Ways Should I Pay Credit Cards or Taxes...

- – Some Known Details About Creating Your Custom...

- – Post-Should I Pay Credit Cards or Taxes First...

- – All about The Benefits and Cons of Bankruptcy

- – How What Regulations Says While Receiving Ba...

Using for credit scores card financial obligation mercy is not as straightforward as requesting your balance be erased. Creditors do not readily use financial obligation mercy, so understanding how to offer your case properly can enhance your chances.

I want to go over any options offered for lowering or resolving my debt." Financial obligation forgiveness is not an automatic alternative; oftentimes, you need to work out with your financial institutions to have a portion of your balance lowered. Charge card companies are commonly open to negotiations or partial mercy if they believe it is their finest possibility to recover several of the cash owed.

Not known Details About Financial Implications Fees for Debt Forgiveness Programs

If they use full mercy, get the agreement in creating before you approve. You may require to submit an official written demand describing your challenge and just how much forgiveness you require and provide paperwork (see following section). To discuss successfully, attempt to recognize the creditors setting and use that to provide a solid instance regarding why they ought to work with you.

Below are one of the most typical errors to avoid in the process: Creditors won't just take your word for it. They require evidence of financial hardship. Always ensure you get confirmation of any forgiveness, settlement, or difficulty strategy in creating. Financial institutions might use much less relief than you need. Negotiate for the very best possible terms.

The longer you wait, the extra costs and interest accumulate, making it tougher to qualify. Debt forgiveness includes legal considerations that borrowers must understand prior to continuing. Customer defense regulations regulate exactly how financial institutions handle mercy and settlement. The following government legislations assist protect customers seeking financial obligation forgiveness: Prohibits harassment and violent debt collection techniques.

The Of Ways Should I Pay Credit Cards or Taxes First? Your Complete Debt Priority Guide : APFSC Guarantees Legal Compliance

Needs creditors to. Forbids financial debt negotiation companies from charging ahead of time costs. Understanding these protections assists stay clear of frauds and unjust lender methods.

This time frame varies by state, commonly between three and 10 years. When the statute of restrictions expires, they generally can not sue you any longer. Nevertheless, making a repayment and even acknowledging the financial debt can restart this clock. Also, also if a lender "fees off" or composes off a financial debt, it does not suggest the financial debt is forgiven.

Some Known Details About Creating Your Custom Should I Pay Credit Cards or Taxes First? Your Complete Debt Priority Guide : APFSC Roadmap

Prior to concurring to any payment plan, it's a great idea to examine the law of restrictions in your state. Legal ramifications of having financial obligation forgivenWhile financial obligation mercy can eliminate monetary concern, it includes possible lawful repercussions: The internal revenue service deals with forgiven financial obligation over $600 as taxable revenue. Borrowers obtain a 1099-C kind and should report the amount when filing taxes.

Below are some of the exemptions and exemptions: If you were insolvent (implying your total debts were higher than your overall assets) at the time of forgiveness, you may leave out some or every one of the terminated debt from your taxable income. You will need to submit Type 982 and attach it to your income tax return.

While not connected to charge card, some pupil finance mercy programs allow debts to be canceled without tax obligation effects. If the forgiven debt was associated with a qualified ranch or service operation, there might be tax exemptions. If you do not receive financial debt forgiveness, there are different debt relief approaches that may benefit your situation.

Post-Should I Pay Credit Cards or Taxes First? Your Complete Debt Priority Guide : APFSC Services Such as Community Resources for Beginners

You request a brand-new finance big sufficient to pay off all your existing credit report card balances. If accepted, you make use of the new finance to repay your bank card, leaving you with just one regular monthly repayment on the combination loan. This simplifies financial obligation monitoring and can conserve you cash on passion.

Most importantly, the company discusses with your financial institutions to lower your rate of interest, dramatically reducing your total financial obligation problem. DMPs might likewise reduce or remove late charges and fines. They are a wonderful debt option for those with poor credit report. When all various other alternatives fail, bankruptcy may be a sensible course to getting rid of frustrating credit scores card financial debt.

Allow's face it, after several years of greater rates, cash doesn't go as much as it made use of to. Regarding 67% of Americans say they're living paycheck to paycheck, according to a 2025 PNC Bank research, which makes it hard to pay down debt. That's specifically true if you're carrying a huge debt balance.

All about The Benefits and Cons of Bankruptcy

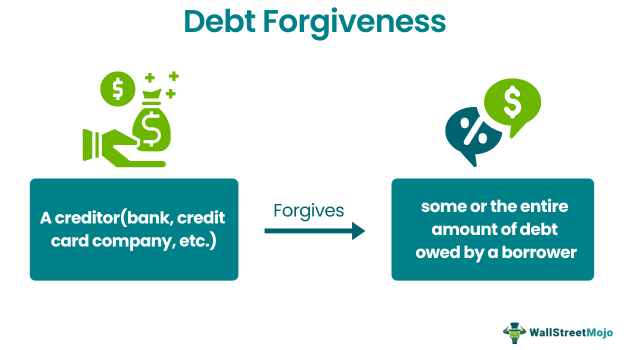

Debt consolidation lendings, financial obligation administration plans and settlement techniques are some techniques you can utilize to reduce your debt. However if you're experiencing a major economic hardship and you've worn down other choices, you may take a look at financial debt forgiveness. Financial obligation forgiveness is when a lender forgives all or several of your impressive balance on a car loan or other credit report account to assist relieve your debt.

Financial debt mercy is when a lending institution concurs to wipe out some or all of your account balance. It's a technique some individuals make use of to reduce financial debts such as debt cards, personal financings and pupil lendings.

The most widely known alternative is Public Service Lending Forgiveness (PSLF), which wipes out staying government loan equilibriums after you work complete time for an eligible employer and make repayments for 10 years.

How What Regulations Says While Receiving Bankruptcy Counseling can Save You Time, Stress, and Money.

That implies any kind of nonprofit health center you owe may be able to offer you with financial debt alleviation. Even more than fifty percent of all united state hospitals supply some type of medical financial obligation alleviation, according to individual solutions support group Buck For, not simply nonprofit ones. These programs, often called charity treatment, lower and even remove medical bills for professional people.

{kind=link}

Table of Contents

- – Not known Details About Financial Implications...

- – The Of Ways Should I Pay Credit Cards or Taxes...

- – Some Known Details About Creating Your Custom...

- – Post-Should I Pay Credit Cards or Taxes First...

- – All about The Benefits and Cons of Bankruptcy

- – How What Regulations Says While Receiving Ba...

Latest Posts

How The Advantages to Consider of Debt Forgiveness can Save You Time, Stress, and Money.

Getting My Economic Impact the Expense of Bankruptcy Counseling To Work

What Does Value of Professional Debt Counseling Mean?

More

Latest Posts

How The Advantages to Consider of Debt Forgiveness can Save You Time, Stress, and Money.

Getting My Economic Impact the Expense of Bankruptcy Counseling To Work

What Does Value of Professional Debt Counseling Mean?